A historic shift is on the horizon

Gospel of Matthew (21:12–13): Jesus went into the temple and drove out all who were buying and selling there; he overturned the tables of the money changers and the benches of those selling doves. And he said to them, “It is written, ‘My house shall be called a house of prayer,’ but you have made it a den of thieves.”

Introduction

Anyone who follows current world events can’t help but shake their head: The Anglo-Saxon “bully” is once again getting dragged into a war he can only lose. In Ukraine, it is already facing an adversary that is showing it the limits of its real power, and now it rubs its eyes in amazement, wondering how it is possible that the “subhumans” in Persia are not voluntarily surrendering and submitting to servitude in the face of the advancing U.S. armada.

Given the actual balance of power (the technological level of Iranian armaments in the fields of ISR and missile technology, the topographical and demographic conditions of Iran, the unity and resolve of the Iranian people, and the active support of very powerful forces such as Russia and China), many rational military advisors have warned USreal that this attack on Iran—which violates international law in every respect—will lead to massive setbacks in their plan to further subjugate the region.

It brings to mind Herodotus, who reports that Croesus (nomen est omen), the king of Lydia (c. 595–546 B.C.), sought the prophecy of the Oracle of Delphi before attacking the Persian Empire under Cyrus II: “Should I go to war against the Persian Empire?” The oracle’s answer was said to be: “If you cross the River Halys, you will destroy a great empire.” Croesus interpreted the ambiguous oracle’s pronouncement according to his own wishes. But in the end, Lydia was conquered by Persia, and not the other way around.

Why this war, and why now?

There are numerous theories regarding the reasons for and timing of this war by USrael against Iran. We would like to add another perspective here.

Many have rightly pointed out that the propaganda-driven justifications for military strikes against Iran are unfounded: Iran poses no military threat to the West, let alone to the United States—its military equipment is purely defensive in nature. Nor is Iran an exporter of terrorist attacks against the West. To the extent that it supports Hezbollah, Ansarallah in Yemen, Iraqi militias, or others, these are not terrorists but liberation forces defending themselves against the colonization of their countries by the West. The argument that the U.S. should have launched a preemptive strike against Iran because American soldiers at bases in the region would also be attacked in the event of an expected Iranian counterattack against an impending Israeli aggression is inherently contradictory and completely confused. An Israeli attack on Iran is only possible with American permission. There can be no question of U.S. self-defense. All these “justifications” are obviously far-fetched.

But in this geostrategic world, nothing happens by chance. So what is really going on?

Explanatory Approaches

In his blog The New Atlas on February 12, 2026, Brian Berletic rightly pointed out that plans for this war have been in place for decades. The strategy of having the U.S. send Israel in first, only to then “come to its aid,” was also part of this plan. The decision to attack Iran has been set in stone for decades. As soon as Iran overthrew the American puppet regime in the 1970s, the U.S. was determined to reverse this. And that is precisely what they have been pursuing ever since. And that is exactly what is currently guiding the Trump administration’s decisions. It is not suddenly making these decisions anew. Rather, this administration just happens to be the political face of the continuity of the agenda at this particular moment. As on previous occasions, Berletic refers to the relevant strategy papers from American think tanks. We have detailed this continuity of the agenda in our three-part article “National Security Strategy – Verbal Cosmetic Changes and No Change of Politicy” (Part I, Part II, Part III).

On March 5, 2026, Wolfgang Bittner also referred once again in our blog to the legendary interview given by four-star General Wesley Clark to Democracy Now! in 2007, in which Iran was listed as the seventh country on the list of nations in the Mediterranean region to be destroyed. Clark said that immediately after the attack on the World Trade Center on September 11, 2001, there was a plan for regime change and wars in the Middle East and Africa. In addition to Afghanistan, seven other countries were listed: Iraq, Syria, Lebanon, Libya, Somalia, Sudan, and finally Iran. The interventions against six of these countries were gradually “worked through”; only Iran remained, and this war is now being waged after years of intrigue, incitement, and sanctions.

This list was compiled by Donald Rumsfeld (Secretary of Defense under President George W. Bush until December 2006) and Paul Wolfowitz (Deputy Secretary of Defense for Policy under George H. W. Bush; in the 1980s, he served as Chief of Staff at the Pentagon under Secretary of Defense Caspar Weinberger. He also held several positions on the U.S. National Security Council).

Lawrence Wilkerson, a retired U.S. Army colonel and former Chief of Staff at the State Department under Secretary of State Colin Powell, pointed out in an interview with Nima R. Alkhorshid (Dialogue Works) on March 10, 2026, that Winston Churchill was already a staunch supporter of the Zionist movement. Churchill saw the establishment of a Jewish colony in Palestine as an opportunity to advance British interests in the Middle East while simultaneously winning over the Jewish diaspora politically. Thanks to his close ties with U.S. politicians, particularly President Harry S. Truman, he was able to influence the political climate in the U.S. regarding the Mandate of Palestine. Here, too, Wilkerson sees a continuity of the agenda beyond this historical context—though this time not only from the U.S. In this conversation, he names names regarding the actual instigators of the current warmongering in West Asia. It is the “usual suspects” who have an interest in destabilization: the usurer oligarchy in London and elsewhere. And there, too, the name Rothschild keeps cropping up.

Rothschild Business Models

In fact, they can be summed up in a fairly simple formula. Throughout history, would-be rulers have faced a problem: to build an army capable of projecting power, they turned productive segments of the population into unproductive warriors (or hired mercenaries) who contributed nothing to their country’s real economy. These soldiers had to be equipped, housed, and fed—at the expense of the rest of the population. This equipment, housing, and food were costly (Napoleon: “An army marches on its stomach.”). Taxes were not enough to cover these costs. What to do?

The gentlemen of the Red Shield were happy to help. But of course, not for free. First, the benefactor takes a discount. So he pays out only a portion of the face value of a loan—e.g., 90%—while the remainder (10%) is withheld. The borrower, however, must pay interest on the full face value. And then there is the question of collateral. So the would-be potentate pledges all his resources to the loan shark. Because, of course, he cannot repay the loan (which the loan shark had factored in from the very beginning), the loan shark subsequently owns all of the country’s resources (including its productive forces—such as the people’s ability to work, their expertise, education, experience, and skills, as well as the organization of the country’s labor)—in perpetuity—and, of course, the interest continues to accrue.

According to the self-serving family history written by Niall Ferguson, the historian hired and paid for this purpose at the time “The House of Rothschild – Money’s Prophets – I, II”, this was precisely their primary business model from the start.

“All modern Wars are a Contention of Purse.”

(Henry Dudas to William Pitt at the outset of the wars against revolutionary France – quoted by Niall Ferguson, History of the Rothschilds, Volume I, p. 84)

This becomes quite clear, for example, in the rise of Nathan Rothschild at the beginning of the 19th century, when he was the most important “financial conduit” between the British government and the battlefields of the continent, where the fate of Europe was decided in 1814 and 1815 (Niall Ferguson, op. cit., p. 85 ff.).

It is well worth taking the time to read Ferguson’s magnum opus in detail—despite all the whitewashing and glossing over (especially when it comes to the present day), one can learn many important things from it that help explain the current state of the world—such as the fact that a lender does not, of course, necessarily have to lend his own money. On the contrary: lending other people’s money helps spread risk—it is enough to establish oneself as a hub in the “money market.” In addition to the important anonymity (“the money market” instead of names and addresses), this leads to additional profits: only part of the interest received from the debtor is passed on to the ultimate creditors. Furthermore, one can also trade in government bonds from all sides, buying them cheaply and reselling them at a higher price.

In this context, a global information network that dwarfs those of individual nations is, of course, helpful—the “neutral” creditor who serves all sides also receives the necessary information from all sides (discretion is, of course, a prerequisite). How this private intelligence network came into being can also be gleaned from the aforementioned work. It is therefore no longer surprising that a certain Mr. Epstein was on excellent terms with the intelligence agencies of all sides, that a certain Mr. Macron was employed by Rothschild & Co, and that a certain Mr. Merz served as chairman of the supervisory board of BlackRock Asset Management Germany from 2016 to 2020.

The picture below speaks louder than a thousand words. (As the educated classes say: “You don’t point a bare finger at clothed people.”)

The worst enemy of global loan sharks

This brief overview of the complex business models of these loan sharks shows that they are fundamentally dependent on finding governments or their leaders who are willing to take on long-term debt on the “money market”—as Germany is currently doing with its so-called “special funds.” But when major nations shift toward creating a sovereign (i.e., not permanently debt-dependent) real economy to provide for their respective populations, this cuts the ground from under the creditors’ feet. Here, then, we see one of the most important reasons for the wars in Ukraine and now against Iran: Russia, China, and Iran are inaccessible to the bloodsuckers. So they must be forced into submission before their policies, oriented toward a sovereign real economy, spread worldwide.

A historical example of how this power struggle between the global financial economy and the real economy in favor of one’s own people was “successfully” waged is the United States.

The Example of the United States

After World War II, the United States of America was by far the world’s largest creditor nation. Today, however, it is the world’s largest debtor nation. The financial oligarchs can therefore say: Mission accomplished.

This shift occurred gradually through a series of economic and political developments and as a result of corresponding decisions by domestic actors. After 1945, the U.S. held a unique position: Europe and Japan had been devastated by the war; the U.S. accounted for about half of global industrial production; it held the lion’s share of the world’s gold reserves; and many countries owed it money. With the international Bretton Woods system (1944), the dollar became the world’s central currency. Other currencies were pegged to the dollar, and the dollar, in turn, to gold. This enabled the U.S. to grant international loans and finance programs such as the Marshall Plan.

Starting in the 1960s, structural changes began: the high costs of the Vietnam War (the Korean War had already played a role here), and the large-scale social programs of the Lyndon B. Johnson administration. Increasing foreign investments by American companies led to more dollars flowing abroad than were coming back through exports.

In 1971, President Richard Nixon was forced to abandon the dollar’s peg to gold due to the already staggering national debt. This led to the collapse of the Bretton Woods system, and as a result, the dollar became a purely fiat currency. The U.S. could now finance deficits much more easily. Other countries continued to hold dollar reserves because the dollar remained the world’s reserve currency.

In the 1980s, under President Ronald Reagan, there were major tax cuts and a sharp rise in military spending. As a result, the national debt grew sharply once again. At the same time, the persistent trade deficit widened: the U.S. imported more than it exported. The difference was financed by capital inflows from Europe and later, particularly, from Japan and China, as these countries continued to purchase large quantities of U.S. government bonds.

As early as the 1950s, a process of globalization and deindustrialization began, which later intensified in various waves (such as during the recession of the 1970s). Much industrial production shifted overseas, first to Mexico and then to China and Southeast Asia. The U.S. transitioned from a real economy to an almost exclusively financial economy.

The rise of financial capital in the 1970s and especially in the 1980s (not only in the United States) meant that profits and power increasingly derived not from the production of goods, but from financial transactions, credit, stock market trading, and capital flows. This was facilitated, for example, by the political decisions made under President Ronald Reagan, which lifted many restrictions on banks and capital movements (deregulation of banking, removal of many capital controls, liberalization of stock markets). This made it much easier to invest capital internationally. Major financial institutions such as Goldman Sachs, JPMorgan Chase, Morgan Stanley, and others began investing globally. Institutions like the International Monetary Fund and the World Bank promoted liberalization and the free movement of capital worldwide.

Key drivers of this development included these two gentlemen:

They played a decisive role in the United States losing its economic sovereignty. The country was now completely under the control of the “financial markets”—and with it, the entire Western world, which not only willingly adopted this system but also did everything in its power to promote and expand it, even to the point of its own deindustrialization.

The Dollar as a Global Currency

Despite all this, the dollar remained the world’s most important currency. Many countries still invest their export surpluses in U.S. Treasury bonds—albeit in significantly decreasing amounts.

The “financial market” (who was that again?) ensured that these increasingly worthless Treasury bonds were purchased. Many banks and financial institutions worldwide are required or choose to hold U.S. Treasury bonds to meet regulatory requirements. For example, the Basel framework, an international set of rules for banks, specifies how much capital and liquidity banks must hold to hedge their risks. The publicly stated goal is to prevent banking crises and make the financial system more stable.

Under the Basel I, Basel II, and Basel III frameworks, a bank’s assets are weighted according to their risk. For many government bonds issued by highly rated countries—particularly the United States—the risk weight is approximately 0%. This means that a bank can hold large quantities of U.S. Treasury securities without having to set aside additional capital. In contrast, banks must hold capital reserves for corporate or personal loans. This is why U.S. government bonds are very attractive to banks from a regulatory perspective. It should be noted, however, that the risk weight of approximately 0% for such debt instruments has no basis in the real economy—quite the opposite. Anyone who cannot repay their debts due to a lack of productivity should actually be considered a high-risk debtor. “The financial market” thus manages, through its regulations and propaganda, to sell such a sham as a real asset. This is the only way to create sustained demand for U.S. government debt.

In this context, the petrodollar must not go unmentioned. After Saudi Arabia promised the U.S. on June 8, 1974, that oil in the Middle East could only be traded in dollars, all countries around the world that relied on oil for their energy supply had to first obtain dollars in order to purchase oil. This has largely secured the creditworthiness of the debtor nation, the U.S., to this day.

Both beneficiaries and puppet masters

What is the purpose of this national debt (apart from the fact that it is used to pay for the state apparatus—that is, the political personnel who run the government)?

For the most recent fully completed fiscal year (FY 2025) in the U.S., the following can be estimated with reasonable accuracy: Government revenue was approximately $5.23 trillion. Interest payments on the national debt were approximately $970 billion. The share of revenue allocated to debt service (interest only—no principal repayment!) thus amounted to roughly 18–19% of total U.S. government revenue. And who receives these funds?

This brings us back to the business model that Niall Ferguson describes in detail across some 1,200 pages of his biography of the Rothschild family. And at the same time, we are also reminded of the old German proverb: “He who pays the piper calls the tune!” The potential for blackmail by loan sharks against the political class—now often referred to as the “Epstein class”—is practically limitless. This is not only exploited by people like casino magnate Adelson, who can presumably put pressure on President Trump, at least in part, with her money. AIPAC & Co., which control the U.S. Congress, also make ample use of it. Ultimately, however, this also affects public finances as a whole. One need only look at the annual spectacle surrounding the respective “U.S. federal government shutdown,” where there is a bitter struggle over the respective spoils. At the same time, however—as mentioned—the entire Western banking sector is also affected by this.

Ein wirklicher Politikwechsel ist in den betroffenen Ländern kaum denkbar, solange dieses globale Erpressungssystem funktioniert.

A specter is haunting the collective West (loosely based on Marx and Engels)

The famous opening lines of Karl Marx and Friedrich Engels’ The Communist Manifesto read: “A specter is haunting Europe—the specter of communism.” The first paragraph continues: “All the powers of old Europe have entered into a holy alliance to exorcise this specter: the Pope and the Tsar, Metternich and Guizot, French Radicals and German police. “

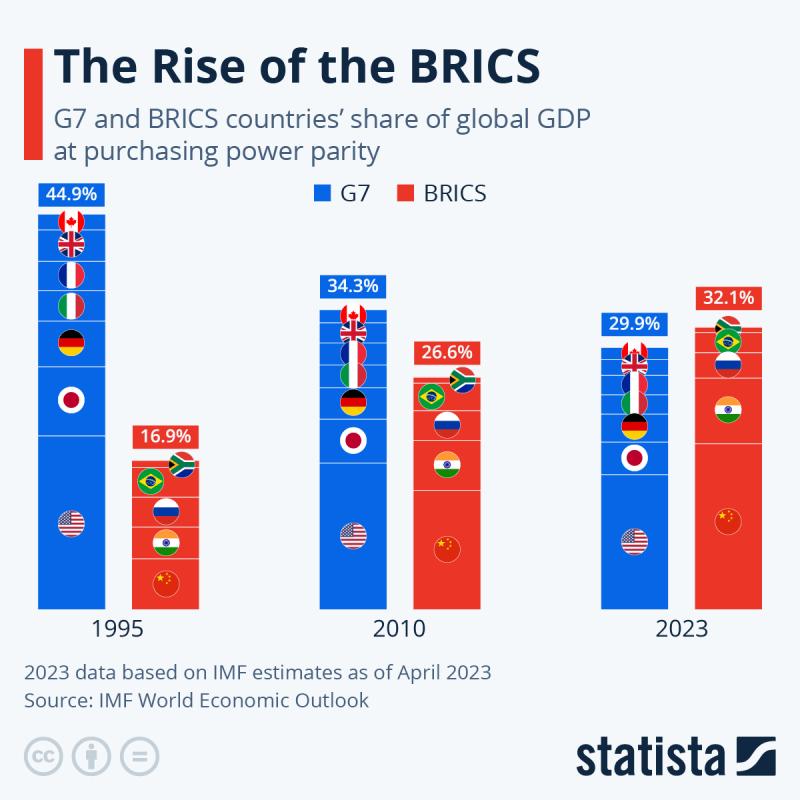

Today, the specter is not communism, but a sovereign real economy modeled on BRICS.

As is well known, the BRICS group is an alliance of emerging economies that strives for a multipolar world order and acts as a counterweight to the Western system. Originally consisting of Brazil, Russia, India, China, and South Africa, the group was expanded on January 1, 2024, and now also includes Egypt, Ethiopia, Iran, the United Arab Emirates, and, since 2025, Indonesia. They represent over 45% of the world’s population and a significant share of global economic output—and the trend is rising.

Turkey applied for BRICS membership on September 3, 2024.

Other interested countries include: Azerbaijan, Bangladesh, Bahrain, Burkina Faso, El Salvador, Gabon, Iraq, Cameroon, Colombia, the Democratic Republic of the Congo, the Republic of the Congo, the Comoros, Kuwait, Laos, Libya, Mali, Myanmar, Nicaragua, North Korea, Pakistan, Palestine, Senegal, Zimbabwe, Sri Lanka, South Sudan, Syria, Tunisia, Venezuela, and the Central African Republic.

What attracts all these countries is the BRICS concept, as the idea of national sovereignty—including in economic terms—is a central component of the BRICS’ self-image. Their summit declarations repeatedly emphasize that states should be able to shape their economic development independently and without external pressure.

For example, the BRICS Johannesburg Declaration (2023) states:

“We reaffirm our commitment to the principles of the United Nations Charter, including the sovereignty, territorial integrity, and political independence of all states. We emphasize the importance of an equitable and inclusive international order in which all countries can pursue their own development paths in accordance with their national circumstances.”

BRICS Johannesburg Declaration (2023)

Another section explicitly emphasizes economic aspects:

“We support an open global economy that enables all countries to achieve their sustainable development and economic transformation, and we oppose unilateral economic measures that are inconsistent with international law.”

BRICS Johannesburg Declaration (2023)

In this context, sustainable development and economic transformation mean that a country’s human and material resources are actually used to provide for its own population, rather than being paid as tribute to colonial masters or loan sharks.

Economic sovereignty requires alternative financial structures. For example, the New Development Bank serves to finance projects without the World Bank or the IMF. National currencies are increasingly being used in trade. Independent payment systems and financial mechanisms are being developed, such as the Cross-Border Interbank Payment System (CIPS) of BRICS partner China.

Countries should exercise control over their own economic development and have the right to determine their own economic policies, pursue their own industrial and development strategies, and regulate their raw materials and markets independently.

This is an indirect challenge to the West’s so-called rules-based order, in which the “rules of the game”—such as the Washington Consensus—are constantly adapted and changed to suit the colonial powers. Rules or institutions that are seen as restricting this scope for action. Thus, the BRICS regularly calls for reforms of the International Monetary Fund (IMF), the World Bank, and international financial rules, because emerging economies have too little influence there on decisions affecting their economies. BRICS documents also criticize measures such as unilateral sanctions, political pressure via financial systems, and extraterritorial economic laws. Thus, the BRICS becomes the voice of the Global South and a platform for equitable economic cooperation—all of this as a counter-model to a global economic order unilaterally dominated by Western loan sharks.

No wonder the former colonial powers fear this development like a looming specter and are doing everything in their power to weaken BRICS—and above all its central pillars, Russia, China, and Iran—or, if possible, to take them completely out of the picture, since they cannot take them over.

Did MAGA want to break out of the vicious cycle?

Intelligent and highly informed individuals such as Alex Krainer have put forward the theory that there were—and still are—forces within the Trump administration (and in the circles pulling the strings behind it) who foresee the impending collapse of the current debt-driven financial system and are attempting to break free from this vicious cycle. The original agenda behind Donald Trump’s slogan “Make America Great Again” (MAGA) was strongly focused on strengthening the real economy—at least in economic policy rhetoric and in several key measures of his first term (2017–2021). The primary focus was on domestic industry, manufacturing, infrastructure, and jobs—that is, sectors of the real economy as opposed to financial speculation.

A key point was bringing industrial production back to the U.S. and criticizing the deindustrialization that had been underway since the 1980s. The aim was to create incentives for companies to resume production in the U.S. Rhetorically, the MAGA strategy explicitly opposed the globalization of the 1990s and 2000s and drew on older American economic traditions such as Alexander Hamilton’s promotion of industry (18th century), economic nationalism, and protectionism.

In this context, reference is made, for example, to Donald Trump’s speech in Riyadh (Saudi Arabia), which he delivered at a summit with Arab and Muslim heads of state. Particularly well-known is the speech delivered at the Arab Islamic American Summit on May 21, 2017, in Riyadh. In it, he did not directly criticize “globalization” as a concept, but rather Western interventionist and nation-building policies, which he linked to the United States’ globalist approach since the 1990s.

On February 14, 2026, U.S. Secretary of State Marco Rubio delivered a speech at the Munich Security Conference that, in addition to incredibly confused remarks about the reestablishment of a neocolonialist world, also contained critical undertones regarding globalization to date:

“Under this illusion—that we were living in a world without borders—we accepted a dogmatic notion of completely free trade, even as other countries protected their markets and subsidized their companies to systematically undercut ours. This led to factories closing, large parts of our society being deindustrialized, millions of jobs being moved overseas, and critical supply chains falling into the hands of rivals and adversaries.”

(...)

“Deindustrialization was not inevitable.

It was a deliberate political decision—a decades-long economic project that robbed our nations of their wealth, their productive capacity, and their independence.

The loss of our control over supply chains was not the result of a healthy global trading system.

It was a foolish and voluntary transformation of our economy that made us dependent.”

Marco Rubio, February 14, 2026, in Munich

It is no coincidence that this passage from the speech is not mentioned in Western media coverage.

The actual policies of the first and second Trump administrations have not yielded any noticeable progress in addressing the critical developments mentioned above. Yet it does seem that at least the speechwriters occasionally made accurate references to these issues.

Russian foreign policy, too, attempted for a certain period of time, with the help of the so-called Anchorage Process, to encourage this segment of U.S. financial circles to change their current course—without success.

Be that as it may: if there was ever a dispute over direction within the circles of the aforementioned financial oligarchy, it now seems to been definitively settled in light of the war against Iran.

An attempt to answer the original question

So how did the warmongers behind the scenes manage to drive the U.S. into this war against Iran? Since 9/11, every American administration has avoided actually launching this war. They have relied on propaganda and sanctions, occasionally encouraging or carrying out military strikes. But a total war like the one we’re seeing now never materialized, even though Netanyahu has been spinning tales for decades that Iran is “on the verge” of building a nuclear bomb and setting the world ablaze.

Was Donald Trump blackmailed (with the Epstein files, by his major donors, or by AIPAC)? This is not a plausible explanation. A system like the American political machine cannot be seriously endangered by a decapitation strike. What about Kennedy? What about Nixon? The system simply replaced the leader and carried on with business as usual. So if Trump were to be overthrown, the continuity of the agenda would continue regardless.

In this case, therefore, the blackmail must have taken on a significantly different dimension. The thesis presented here assumes that the dominant financial oligarchy held a gun to the heads of the dissenters in American decision-making circles: either you wage this war now, or we’ll pull the plug on you—meaning that at the next auction for U.S. Treasury bonds, there will be no bids from our side.

The reason for this is likely that “the specter” of the BRICS system is growing and growing, and Iran is playing a decisive role in this. For if Iran, with the help of China and Russia, succeeds in decisively determining the world’s energy supply, the financial sharks of the West will lose their decisive leverage. Therefore, Iran must be destroyed.

The time is ripe because Russia is still tied down in Ukraine and time is of the essence, as China is gaining more and more influence in Iran and thus throughout West Asia.

If USrael cannot win this war (which was foreseeable from the start and is now becoming clear), then these financial sharks couldn’t care less. Europe has committed collective suicide twice, and both times they financed the carnage from all sides. They don’t care about the death of entire nations or regions—after all, they can pick up the pieces, offer themselves as lenders for reconstruction, and in the process also dictate the terms, both financially and politically. The looming destruction of the State of Israel in its current colonialist form, the destruction of American bases and the Arab vassal states, is accepted with approval. The significant damage in Iran is intentional.

What will the outcome look like?

No one has a crystal ball to show us the future. But it is becoming clear that US-Israeli power projection in West Asia is running out of steam. The world’s supply of oil from this region will in the future be determined by Iran and its allies. Iran has already effectively erected a customs barrier in the Strait of Hormuz, which could spell the end of the petrodollar: only those who pay in yuan or another BRICS currency, or who use the Chinese Cross-Border Interbank Payment System (CIPS), are allowed to pass.

It appears that Iran might succeed in accomplishing what Jesus attempted, according to the New Testament legend cited above: definitively driving the money changers out of the temple and thereby undermining the foundation of the Old Testament-era power structure. It is to be hoped that this can be achieved without the former rulers resorting to the Samson option.

«A historic shift is on the horizon»