Fed Considers Gold Reserve Revaluation

On February 3, 2025, President Trump signed an executive order directing the creation of a sovereign wealth fund within one year. Standing beside him, Treasury Secretary Scott Bessent told reporters, “Within the next 12 months, we are going to monetize the US balance sheet for the American people. We are going to put the assets to work”.

His brief remarks immediately sparked speculation over which assets he was referring to. Four days later, the Financial Times suggested the target might be gold: “Some hedge fund contemporaries of Scott Bessent, the hedgie-turned-U.S. Treasury secretary, are speculating about a revaluation of America’s gold stocks.”

Gold monetisation means transforming an inert reserve asset into an active financial instrument that can be used to fund government operations, settle debt, or stabilise the economy. It does not necessarily require selling the gold — in many cases, the asset remains in reserve, but its value is “activated” to provide liquidity.

On August 1, Colin Weiss, a senior economist at the Federal Reserve, reignited the debate by publishing an article on gold revaluation — the first time in modern history the institution had publicly addressed the subject.

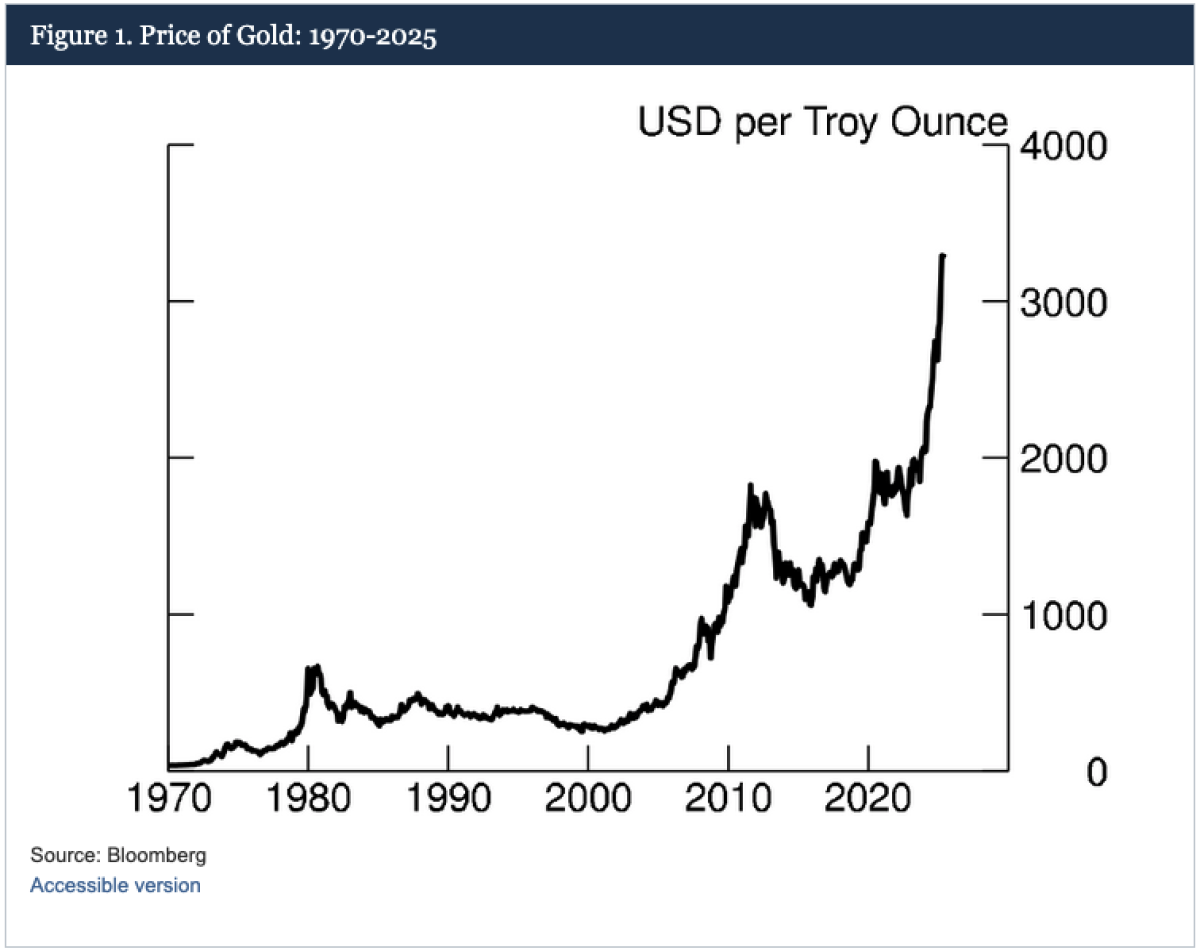

The United States officially holds the largest gold reserves in the world: 261.5 million troy ounces, or more than 8,133 tons. The gold belongs to the U.S. Treasury but is carried on the Fed’s balance sheet at its historical cost of $42.22 per ounce. These holdings were acquired before 1990, long before their market value soared.

At today’s market price of about $3,300 per ounce, the reserves would show an unrealized gain of about $850 billion — around 3% of GDP — that could be mobilized without raising taxes, issuing new debt, or selling a single ounce. In times of fiscal stress, such an accounting shift could prove politically tempting.

The Fed document reviews five countries that have adopted similar measures over the past 30 years. It does not comment on the merits of such a move for the US, but warns that it is not a panacea for the country's $37 trillion debt: “While reducing the debt stock using revaluation proceeds improves the fiscal situation at the margin, it may not address larger structural challenges.”

The release of this publication signals a remarkable return of gold — and its monetary role — to the heart of economic policy debates. Since President Nixon reneged on the U.S. commitment to convert dollars into gold at $35 per ounce in 1971, the metal has been largely absent from official discourse, often dismissed as a “barbaric relic.”

As Jim Rickards notes, gold has virtually disappeared from traditional economic debates for over 50 years. It is seldom mentioned in textbooks, rarely discussed in academic or political circles, and often ignored by economists. Many Americans are not even aware that it once served as a guarantee for the dollar. This collective amnesia serves a single purpose: to preserve the government's monopoly over money creation.

The greatest power a central bank holds is the ability to back its currency with nothing more than public confidence. By creating money out of thin air, it can erode citizens’ savings through inflation — effectively confiscating wealth by devaluing the currency. This power is even greater when the currency is a global reserve, as with the U.S. dollar.

Yet the United States has arguably overused this privilege : sweeping sanctions, persistent deficits, surging debt, and inflation have all undermined trust. Since 1971, the price of gold has increased by a factor of about 78 — rising from $42 to roughly $3,300 per ounce — an average annual gain of 8.4%, more than double the average U.S. inflation rate of 3.9%.

If the Fed and the Treasury are now openly discussing gold, it may signal that policymakers are running out of politically viable options. The arguments in favor of a revaluation of gold are growing stronger, signaling its return as a monetary asset.

According to BofA strategist Michael Hartnett, “secular inflation, debt, and currency debasement may mathematically force central banks to revalue gold to offset fiat reserve losses”— a move likely bullish for gold and bearish for the dollar.

«Fed Considers Gold Reserve Revaluation»